Is Your Retirement Portfolio Built for an Institution or for You?

Why the investment model for institutions is failing retirees.

After going through the meticulous process of financial discovery, risk tolerance testing, and goal setting, it can be frustrating to realize that your carefully tailored retirement strategy may be resting on a flawed foundation. Whether your advisor places you in a bucket system, an actively managed program, or a static allocation, the underlying reality is that most individual retirement portfolios are built upon a model designed for a very different type of investor: the short-term institutional fund.

The Institutional Bias in Modern Portfolio Theory

The core issue lies in the pervasive use of a particular application of Modern Portfolio Theory (MPT). Institutional investors, such as endowments or pension funds, often require liquidity to plan for large, irregular short-term withdrawals (e.g., a university needing to fund a major capital expense or a pension fund covering a sudden spike in early retirements).

To meet this need, the primary variable used to define "risk" in their portfolio model is volatility (standard deviation of returns).1 A high-volatility asset is deemed "risky" because its value could drop sharply just before a required large withdrawal, jeopardizing the fund's short-term ability to meet its obligations.

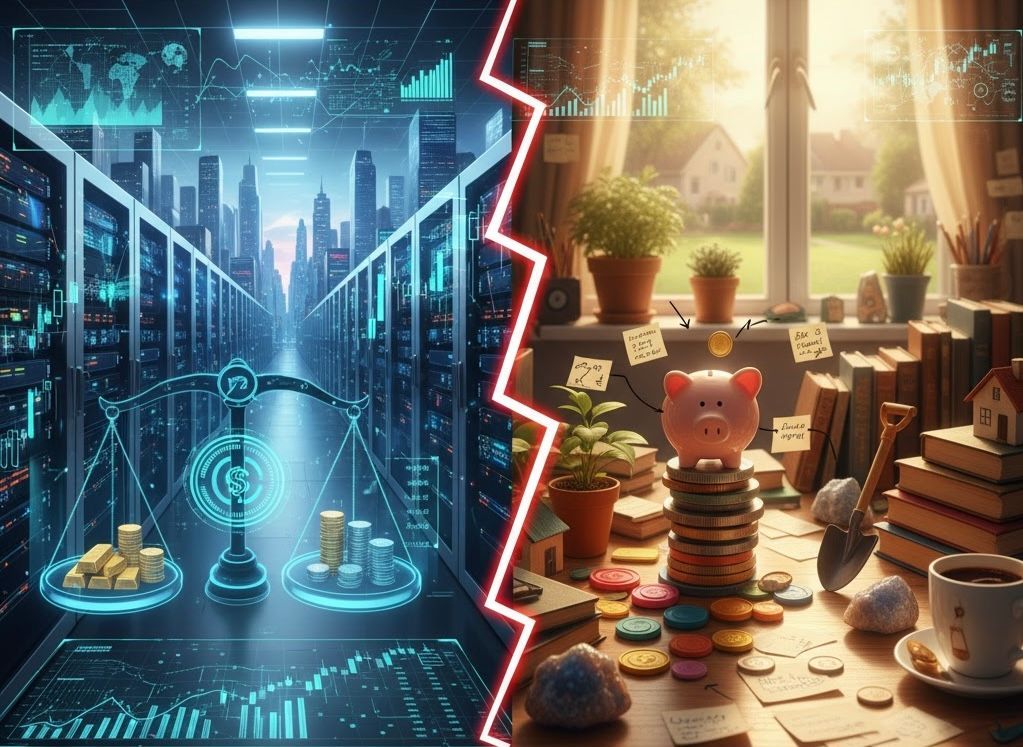

The Mismatch: Individual vs. Institution

This short-term, volatility-based risk assessment is then applied wholesale to the individual retirement portfolio, despite the stark difference in an individual's financial needs.

Institutional Portfolio:

Time Horizon: Short-to- Intermediate

Withdrawal Pattern: Large, irregular lump sums

Primary Risk: Volatility - inability to meet a large near-term obligation

Individual Retirement Portfolio:

Time Horizon: Long-Term (often 20-30 years)

Withdrawal Pattern: Small, proportional regular income stream

Primary Risk: Longevity and Inflation -

running out of money

The Cost of Short-Term Risk Management

By treating a 30-year retirement portfolio as if it needed the same volatility controls as a 3-year institutional fund, the individual ends up with a conservative bias that severely impacts long-term growth.

This bias forces the inclusion of more defensive, lower-growth assets—often in higher proportions than necessary—leading to a diluted income stream. The consequence is a demonstrable sacrifice of 2-4% in total annual returns over the portfolio's lifetime.

While 2-4% might seem minor, the compounding effect over decades is catastrophic. This forced underperformance leads to a cascade of negative outcomes for the retiree:

1. Delayed Retirement: The individual must work longer to accumulate a larger principal to compensate for the lower expected return.

2. Higher Investment Requirement: A much greater total amount of money must be saved to achieve the same future income goal.

3. Lower Income Streams: The portfolio simply generates less available income, leading to a diminished lifestyle in retirement.

4. Reduced Annual Increases: The lack of robust growth limits the ability to increase annual withdrawals to keep pace with the true rate of inflation.

5. Portfolio Shrinkage: The portfolio gradually becomes a depreciating asset. Instead of a stable or growing asset base, the retiree is constantly forced into the required sale of assets to meet their annual income needs, often leaving the portfolio vulnerable to being outpaced by inflation.

A Call for a Long-Term Perspective

The current system, while providing the illusion of safety through volatility management, inadvertently introduces the far greater real-world risk: the risk of outliving your money or experiencing a significant drop in purchasing power due to inflation.

The challenge for the financial industry is to transition from a model obsessed with short-term price swings to one focused on long-term capital preservation and growth in real (inflation-adjusted) terms. An individual's retirement is a decades-long endeavor, and the investment strategy should reflect the resilience and growth potential of that long-term horizon, not the defensive positioning of a short-term institutional checkbook.

A portfolio strategy to address this problem.

share this

Related Articles