Articles

Unlocking Private FUNDS: The Income, Net Worth, or Professional Criteria Required to Become an Accredited Investor

Your Portfolio Must Cover These 4 Risks for a Secure Retirement.

Explore POPULAR Portfolio Benchmarks: From Income to Growth

This is a subtitle for your new post

How to Target Growth While Protecting Your Future

Stop the Drain: The Critical Math of Withdrawal Rates vs. Portfolio Income

Individual retirement portfolios often use a short-term institutional model, sacrificing returns for volatility control and delaying retirement.

Trading safety for high returns? Traditional diversification costs you growth.

Discover Nerat Capital’s Strategy: for security & growth to optimize your retirement.

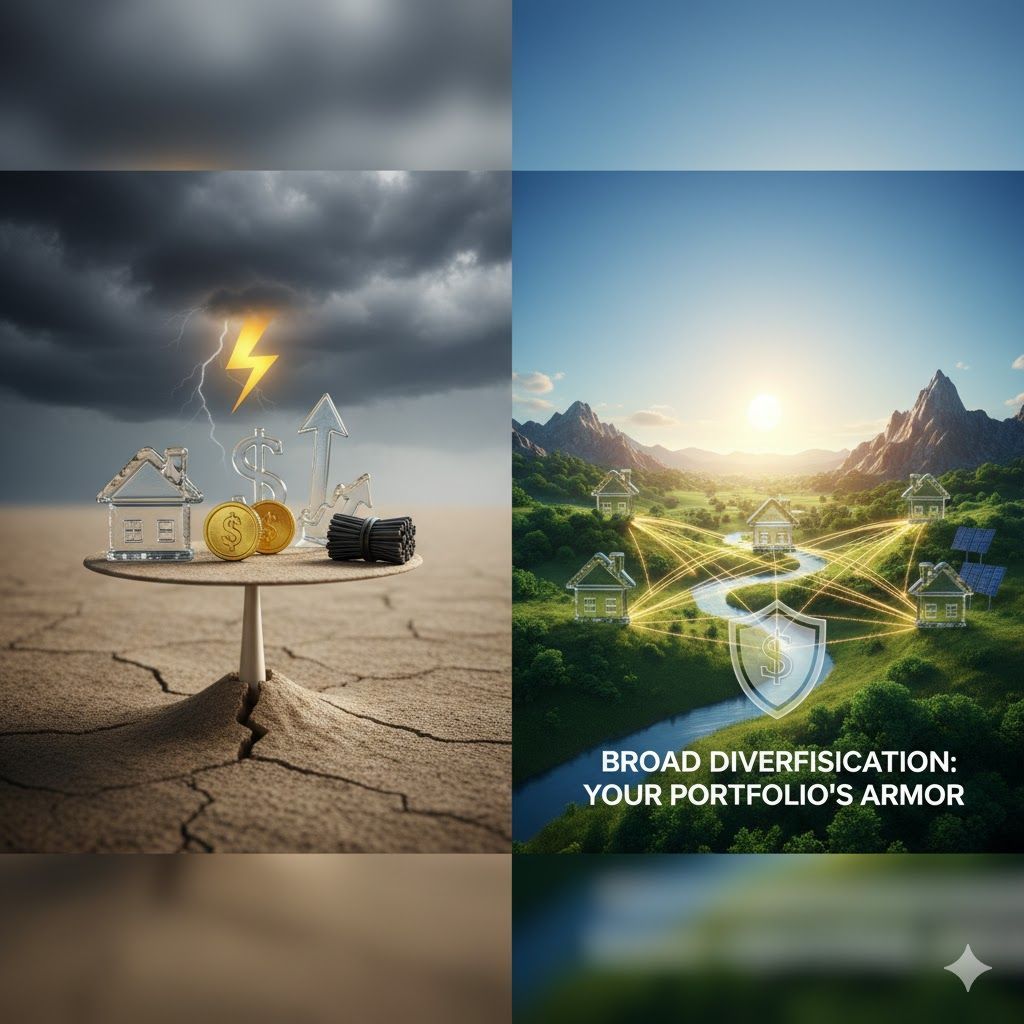

Protecting Your Portfolio From Loss

Get more OUT OF YOUR IRA through consolidation